At-a-Glance: Dual pricing shows a cash price and a card price so retailers can offset the cost of acceptance transparently. With clear signage, correct POS settings, and a simple staff script, you can cut processing costs while keeping checkout friendly.

If card fees quietly erode your retail margins every month, you are not alone. Many shop owners watch 2–4% of card sales disappear to processing costs and assume it is simply the price of doing business. It does not have to be. Dual pricing gives shoppers a clear choice between a cash price and a card price, letting you recover acceptance costs without raising shelf prices across the board. Done well, it is transparent, compliant, and barely noticed by customers. Done poorly, it creates confusion at the register. This guide walks through a practical retail rollout: how the model works, how to configure your retail POS system, what signage and receipts must say, and how to coach your team so the program runs smoothly from day one.

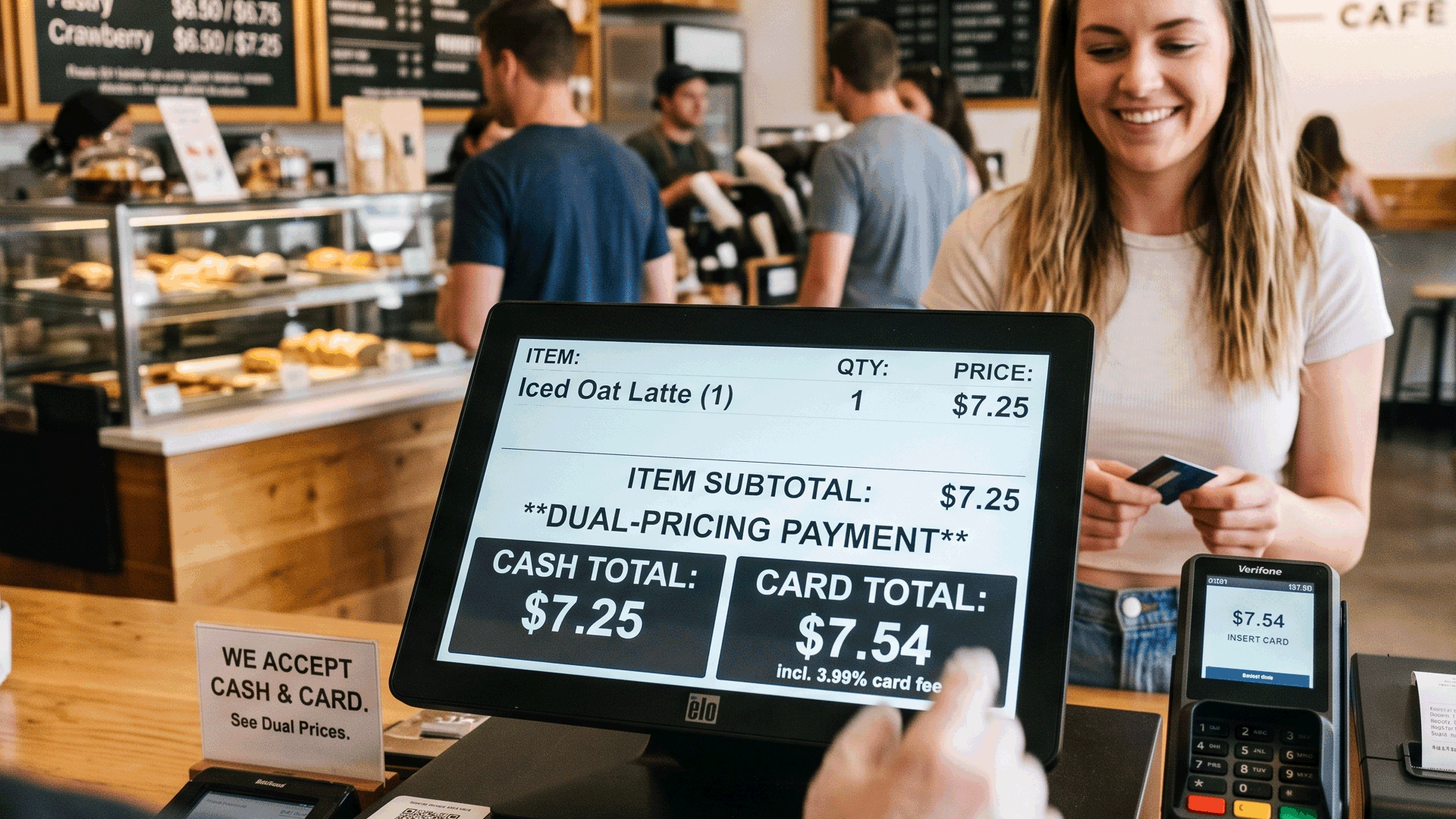

What Dual Pricing Means for Retail

Dual pricing displays two prices for every item or at checkout: a lower cash price and a card price that reflects the cost of card acceptance. Unlike a vague “surcharge,” dual pricing frames the choice positively—customers paying cash get a discount. The difference is usually small per transaction but adds up to meaningful savings across a month of card volume.

Why Retailers Adopt It

Retailers adopt dual pricing to protect thin margins, keep shelf prices competitive, and make the cost of card acceptance visible rather than buried. It also gives price-sensitive shoppers a way to save, which many appreciate.

Your Retail Rollout Checklist

Configure your POS to display both prices, post compliant signage at the entrance and register, update receipts to show the pricing applied, and train staff on a short, friendly explanation. Test the full flow before going live.

Signage, Receipts & Compliance

Signage must clearly disclose that a card price differs from the cash price, and receipts should reflect the actual price paid. Requirements vary by card brand and jurisdiction, so confirm current rules before launch.

A Real-World Retail Scenario

A boutique with $40,000 in monthly card volume recovers a significant share of processing costs within the first month of a clean dual-pricing rollout—without customer complaints, because the signage and staff script set expectations up front.

Common Mistakes to Avoid

The biggest mistakes are unclear signage, inconsistent register behavior, and untrained staff who cannot explain the program. Each creates friction; all are avoidable with preparation.

How Media Payments Group Helps

Media Payments Group configures dual pricing correctly inside your retail POS, supplies compliant signage guidance, and trains your team so the rollout is smooth. We focus on transparent setups that hold up to scrutiny and keep your checkout experience friendly.

We can also model your current processing costs against a dual-pricing scenario so you see the impact before you commit, and we support you after launch as questions come up.

Practical Takeaways

- Dual pricing offsets acceptance costs transparently with a cash price and a card price.

- Success depends on clear signage, correct POS configuration, and a trained team.

- Confirm current card-brand and jurisdiction requirements before launch.

Dual pricing is one of the most direct ways for a retailer to protect margins without raising shelf prices—but only when it is rolled out cleanly. If you would like help configuring your POS, getting signage right, and coaching your team, Media Payments Group can guide the whole process.

Frequently Asked Questions

Is dual pricing the same as surcharging? No. Dual pricing presents a cash price and a card price as a choice, while surcharging adds a fee on top of one price. The rules and disclosures differ.

Will customers be annoyed? When signage and staff scripts are clear, most customers understand and many appreciate the cash-discount option.

Do I need special hardware? Usually not—most modern POS systems support dual pricing with the right configuration.

Is it compliant everywhere? Requirements vary by card brand and location. Confirm current rules before launching.