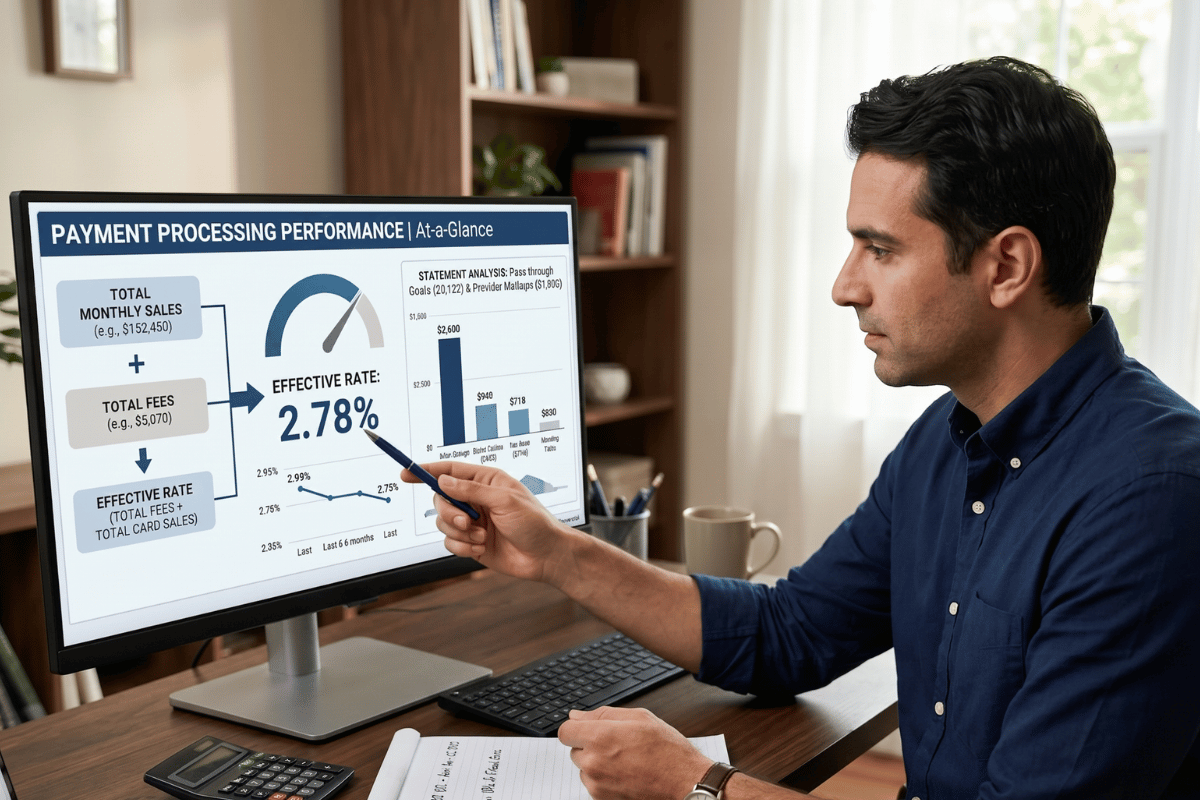

At‑a‑Glance: Your statement lists pass‑through costs (interchange, assessments) and provider markups (basis points, per‑item, monthly fees). Focus on effective rate—total fees ÷ total card sales—and the levers that actually move it.

Interchange vs. Markups

- Interchange & assessments: set by card brands and banks; vary by card type and entry method.

- Provider markups: the negotiable part—basis points, per‑item, and monthly platform fees.

Reading Your Statement

- Locate total card sales, total fees, and deposits.

- Identify pricing model (interchange‑plus, flat/blended, subscription).

- Watch for add‑ons: PCI, gateway, batch, chargeback fees.

Levers to Lower Your Effective Rate

- Optimize acceptance: EMV/tap over keyed entries; capture AVS online.

- Match pricing model to ticket size: small tickets benefit from lower per‑item; large tickets from fewer bps.

- Consider dual pricing: present a cash price and a card price to offset costs.

- Use ACH for invoices/large orders where appropriate.

Beyond Rates: Operational Wins

- Reduce refunds and disputes with clearer policies and EMV.

- Train staff to avoid avoidable downgrades (missing data, late batches).

How MPG Helps

- Statement reviews that explain, not confuse.

- Programs for dual pricing and ACH with training and templates.

- US‑based support to tune your setup over time.

FAQ

Is a lower headline rate always better? Not if it raises downgrades or per‑item costs. Measure effective rate monthly.

Can I negotiate interchange? No—but you can qualify for better categories by submitting the right data.